Read

Gur

☰

Explore

Log in

Create new account

Upload

×

Download

No category

Global Investment Holdings

Aydınlatma Sistemleri Uygulamaları

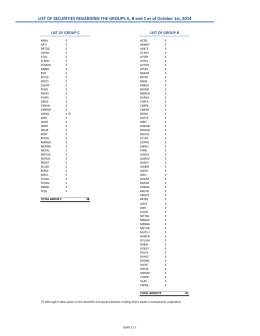

LIST OF SECURITIES REGARDING THE GROUPS A, B and C as of

Türk Traktör

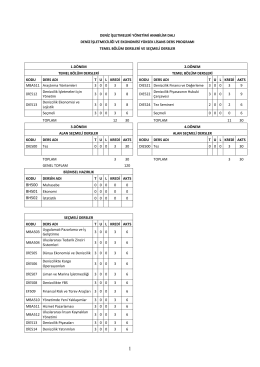

Deniz İșletmeciliği ve Ekonomisi Yüksek Lisans Programı

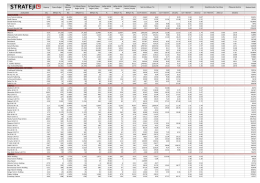

Şirketler Monitörü - Strateji Menkul Değerler

media - Doğan Holding

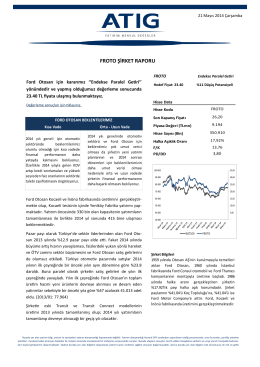

Ford Otosan şirket raporumuza ulaşmak için lütfen tıklayınız

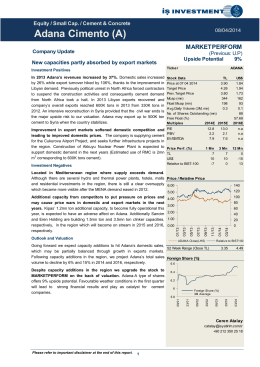

Adana Cimento (A)

araştırma - Garanti Yatırım

BİRİNCİ LİSTE A. KDV İSTİSNASINDAN YARARLANACAK YETKİLİ

Döküm İndir - Global Yatırım Holding

Fundamentální analýza Erste Bank

2. piyasa riski

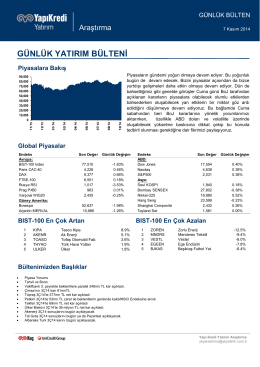

günlük yatırım bülteni

Doç. Dr. Osman AKBA - Dicle Üniversitesi

Parallel Distribution

Incoming pazarının liderleri belli oldu

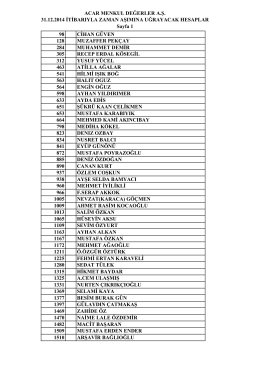

31-12-2014 itibariyle Zamanaşımına Uğrayacak Hesaplar Listesi

Hisse Senedi Stratejisi

Dr. Süleyman SAK`ın Dilekçesi için tıklayınız

Průběh nakupování akcií společnosti O2 Czech Republic as Course

İndir - Global Yatırım Holding