Read

Gur

☰

Explore

Log in

Create new account

Upload

×

Download

No category

September 2014 - Türk Telekom Investor Relations

öğrenci kabulüne ilişkin sınavlarla ilgili detaylı

2012 MATADOR Industries, a.s. Výročná správa Annual report

EFRS 5. DEMİR ÇELİK SEMPOZYUMU 22

Dış Basında İstanbul - İstanbul Büyükşehir Belediyesi

Turkish Automotive Industry December 2013 Gündüz

Akıllı yapı cepheleri ve sürdürülebilirlik

İntrakraniyal aterosklerotik hastalık tanı ve tedavisi

Kapı Katalogu

Modern tesis tasarımını deneyimleyin

Report Title

Principles of Economics, Case/Fair/Oster, 10e

Application Form

stáhnout pdf

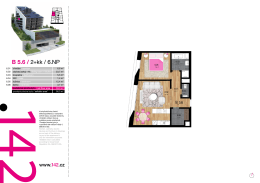

B 5.6 / 2+kk / 6.NP

Attachment to the draft Resolution of the Ordinary

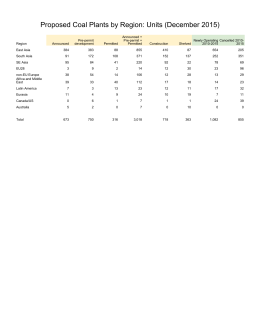

Proposed Coal Plants by Region: Units (December 2015)

Mülkiyet ve işletme maliyeti

spali

Price Stability and Growth in Turkey

Beli Manastir

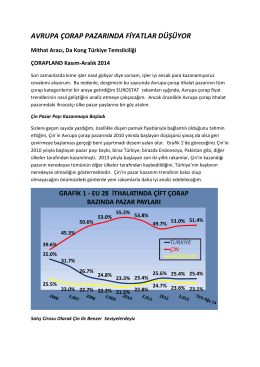

avrupa çorap pazarında fiyatlar düşüyor

VOJVOĐANSKI BOKSERSKI SAVEZ BILTEN TAKMIČENJA