Read

Gur

☰

Explore Categories

Sign in

Sign up

Upload

×

Download

No category

ODAS ODA IPO Projections 23052014

ODAS Varsayımlar Gerçekleşme Raporu

ODAS Varsayımlar Gerçekleşme Raporu

3.Çeyrek Faaliyet Raporu

ODAS - Bizim Menkul Değerler

KPD - Nadaní dospělí.key

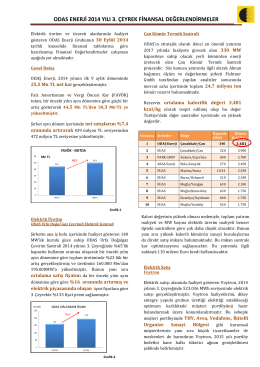

3.Çeyrek Finansal Değerlendirmeler

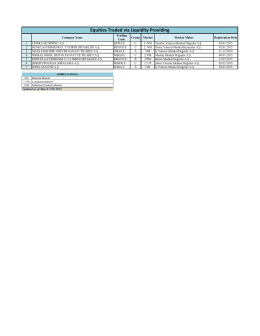

Equities Traded via Liquidity Providing

2013 yılı faaliyet raporu

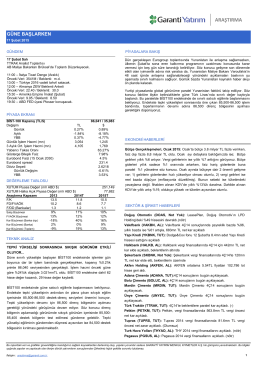

araştırma - Garanti Yatırım

DIVIDEND PLAYS - 2015

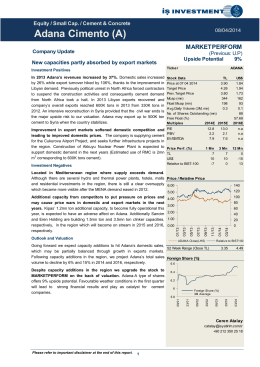

Adana Cimento (A)

2.Çeyrek Finansal Tablolar