Read

Gur

☰

Explore

Log in

Create new account

Upload

×

Download

No category

15.04.2014

Tarih 21.07.2014

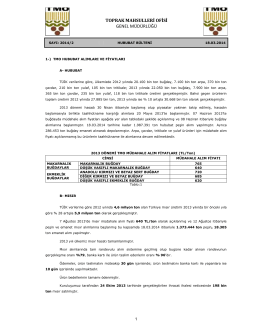

Tarih 18.03.2014

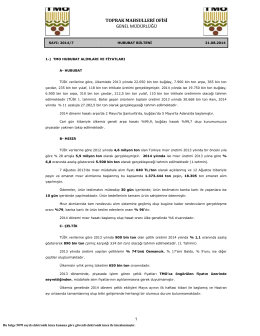

Tarih 21.08.2014

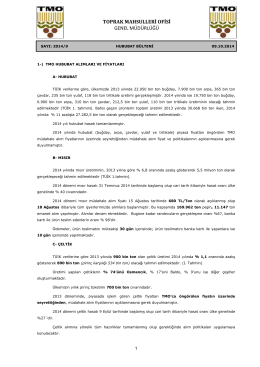

Tarih 09.10.2014

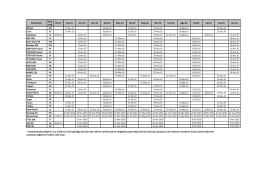

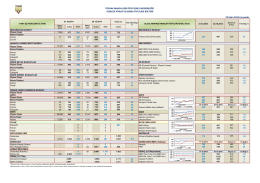

Enstrüman Kısa Kod Eki.15 Kas.15 Ara.15 Oca.16 Şub.16 Mar.16

Jedálny lístok

tıbbi görüntüleme teknikleri

Tarih 24.06.2014

Prague City Report - Jones Lang LaSalle

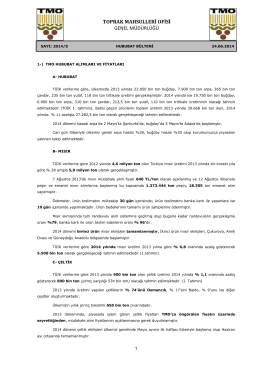

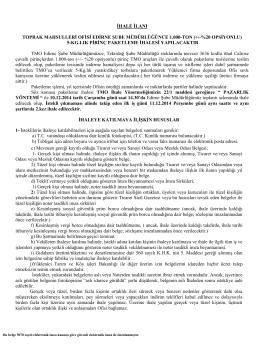

TOPRAK MAHSULLERİ OFİSİ

IIzlaganje i diskusija po referatu do 15 minuta

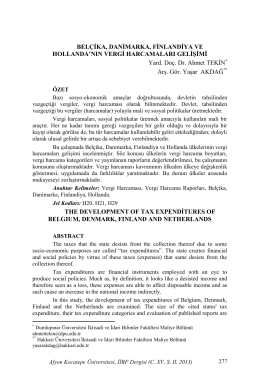

BELÇİKA, DANİMARKA, FİNLANDİYA VE HOLLANDA`NIN VERGİ

IMMOPARK Košice – dôležitý ťahúň Košického kraja

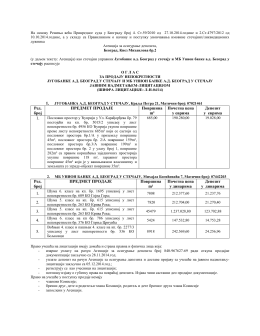

Ред. број ПРЕДМЕТ ПРОДАЈЕ Површина m² Почетна цена у

information frictions and the effects of news media bias on

16.06.2013. – Nedelja / Sunday DOLAZAK I

Teknolojik Ürün Yatırım Destek Programı İle İlgili Sunum Dosyasını

5 Beskydských vrcholů očima náhradníka.

Araştırmacı: Külçe MgB - Bülent Ecevit Üniversitesi

GRUP: 3116

TOPRAK MAHSULLERİ OFİSİ GENEL MÜDÜRLÜĞÜ GÜNLÜK

záznam: Světová mlékařská situace 2013