Read

Gur

☰

Explore

Log in

Create new account

Upload

×

Download

No category

document

Více

Prva CFO konferencija u Republici Srbiji a CFO

Pogledaj - Nova Banka

Vodič za investitore - Privredna komora Beograda

Pobierz Monitor Ubezpieczeniowy

Podsticaji dižu investicioni potencijal na milijardu evra

Sprawozdanie z działalności GRUPY KAPITAŁOWEJ

Milli Reasürans Faaliyet Raporu 2013

16, Sayı: 2, Yıl: 2014, Sayfa: 193-212 ISSN: 1302-328

Биографије учесника

Биографије учесника

Dünya Bankası Küresel Ekonomik Beklentiler Raporu

13 EKİM 2014 - Ekonomi Gazetesi

Attitudes Towards the Teaching Profession - ajesi

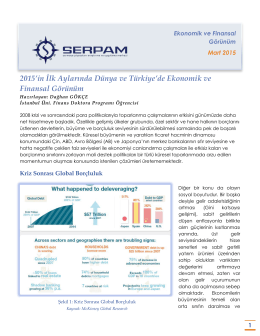

2015`in İlk Aylarında Dünya ve Türkiye`de Ekonomik ve Finansal

Bakterilerde glutatyon ve önemi Glutathione in bacteria and its

R+F Optiline/Plano

Jugoistočna Evropa

anna nagar times

raiffeisen bank polska sa

Opis techniczny WIeluń dom kulturyPW

GENEL TASNİF Page 1