Read

Gur

☰

Explore Categories

Sign in

Sign up

Upload

×

Download

No category

Burak Saltoglu - Department of Economics

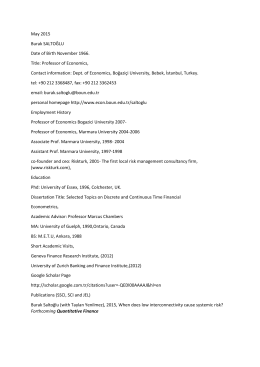

May 2015 Burak SALTOĞLU Date of Birth November 1966. Title

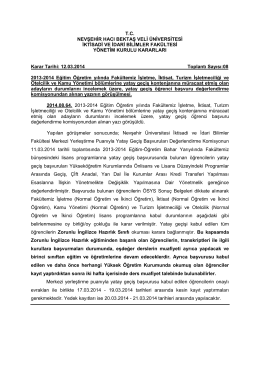

T.C. NEVŞEHİR HACI BEKTAŞ VELİ ÜNİVERSİTESİ İKTİSADİ VE

Absorption Capacity of Turkey 4

sempozyum programı - Atatürk Araştırma Merkezi

Econfin-Math_Review-Syllabus - ECONFIN, Economics and Finance

Devamı İçin Tıklayın

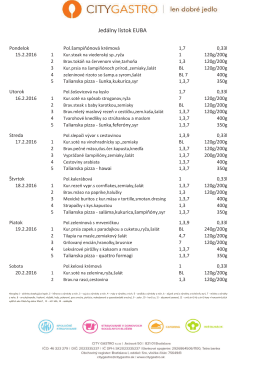

Týždenné menu

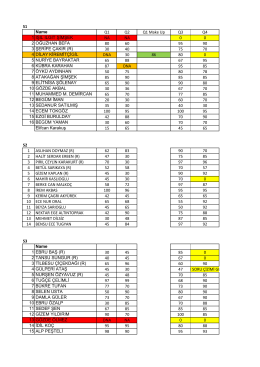

S1 Name Q1 Q2 Q1 Make Up Q3 Q4 1 IŞIL ILGIT ŞİMŞEK NA NA 0

RiskTürk Eğitim Kataloğu 2015 1. Dönem

2014 Yılı II. Dönem Eğitim Kataloğu

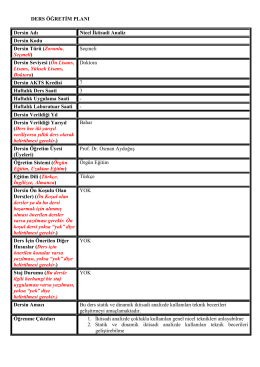

Nicel İktisadi Analiz

RiskTürk Eğitim Kataloğu 2015 1. Dönem