Read

Gur

☰

Explore

Log in

Create new account

Upload

×

Download

No category

To: [Company Name] - BDK Advokati/Attorneys at Law

poreska prijava obrazac opp-pn-2

PROPISI

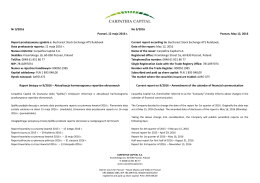

Nr 9/2016 Poznań, 12 maja 2016 r. Raport przekazywany zgodnie z

Udhezim_Administrativ_16_2009 - Administrata Tatimore e Kosovës

Nabycie akcji własnych - Bucharest Stock Exchange

Personal PDF File - Ankara Üniversitesi

Rafinat 2 SDS - HIP Petrohemija

Preuzmite bilten - Karanovic & Nikolic

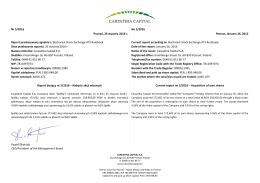

Nr 7/2016 Poznań, 23 lutego 2016 r. Raport przekazywany zgodnie z

Newsletter Confida Consulting JAN 2015

Kosovo: Savladavanje prepreka po političko učešće žena

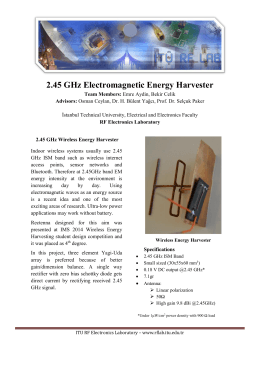

2.45 GHz Microwave Harvester

Slavisa Orlovic- Problemi sa izbornim sistemom u Srbiji

Vitra Karo Yenilikler 2014

SHY M Denetleme Raporu - Sivil Havacılık Genel Müdürlüğü

1. WBL city project doo Banja Luka , kao korisnik koncesije, kojeg

English version on page 9 18. júna 2012 Reforma legislatívy

information about competition