Read

Gur

☰

Explore

Log in

Create new account

Upload

×

Download

No category

2014: 2. Quarter Results

Araştırma. 2

8. Wirusy - Chemia bioorganiczna

IATA kargo acentelerinin telefon ve faks numaraları

DERS KODU TÜRKÇE DERS ADI İNGİLİZCE DERS ADI YARIYIL

zur Dokumentation der 5. Euroregionalen Konferenz

Resmî Gazete Sayfa 1 / 2 Başbakanlık Mevzuatı Geliştirme ve Yayın

BOYUT GÜVENLİK - GENEL REFERANS LİSTEMİZx

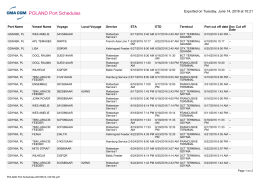

POLAND Port Schedules

Kurumsal Finansman Sunumu

Výroční zpráva

Orta Karadeniz Bölgesi`nde Kooperatifçilik Konferansı

Oral besin provokasyon testi sırasında gelişen reaksiyonların sıklığı

Development of Rural Areas through Enterprise

Giyilebilir Teknolojinin Lüks Tüketim Pazarında

Modül Bilgi Sayfaları

tıklayınız.

Further Information

Tam Metin - Posseible Düşünme Dergisi

CGC Rail Ürün Kataloğu

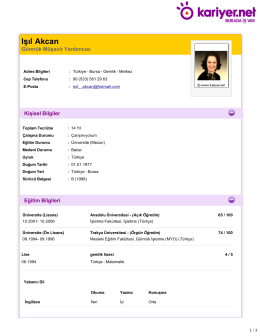

ışık akcan-gümrük müşavir yardımcısı

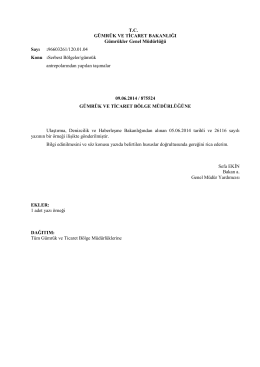

Serbest bölgelerden antrepolara, antrepo ve serbest bölgelerden

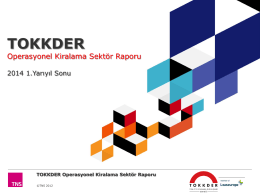

Operasyonel Kiralama Sektör Raporu Sunumu – 2014