Read

Gur

☰

Explore Categories

Sign in

Sign up

Upload

×

Download

No category

Turkish Brokerage Industry 2013 Review (May 2014)

BROKARAGE RAPOR ICSF G025260.indd

Türk Traktör

Brochure EFQM

Emilia Klepczarek - Towarzystwo Ekonomistów Polskich

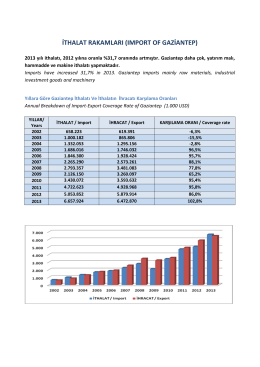

ithalat rakamları (ımport of gaziantep)

mba programı eğitim

C onseil en stratégie pour investisseurs institutionnels

Gümrük Genel Tebliği (Tarife- Sınıflandırma Kararları) (Seri No: 17)

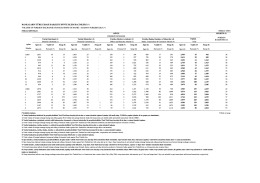

(Million USD) BANKALARIN TÜRK L RASI KAR ŞILIĞI DÖV

Son 5 Yılda Borsadaki Yabancı Yatırımcı Sayısı

Yatırımcılar için Borsa İstanbul

Türkiye Sermaye piyasası Raporu 2013