Read

Gur

☰

Explore Categories

Sign in

Sign up

Upload

×

Download

No category

Network structures of the European stock markets

05 15 Svoboda-Ourednicek + RS - Urbánní a regionální laboratoř

DRUGA KOLONIA?

štvorec v kruhu - Art Film Festival

Scientific Papers 35 (3/2015)

HPV Negative Seborrheic Keratosis of Genital Area Genital Bölgede

17 nisan 1

Raut moderni smery

an application on the brand of talent management

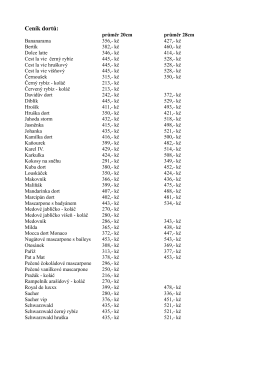

Ceník dortů:

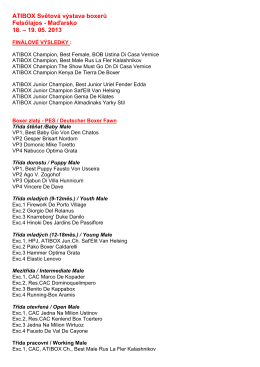

ATIBOX Světová výstava boxerů Felsőlajos

TRŽIŠTE NOVCA I KAPITALA 03

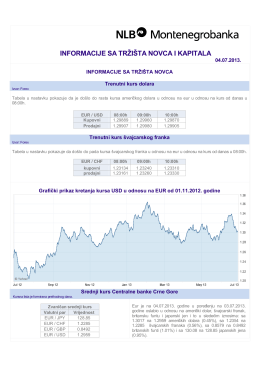

Preuzmite izvještaj - NLB Montenegrobanka