Read

Gur

☰

Explore

Log in

Create new account

Upload

×

Download

No category

here - fbme limited

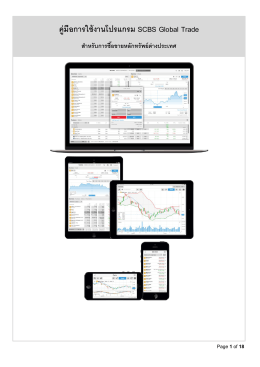

คู่มือการใช้งานโปรแกรม SCBS Global Trade

SS. Cyril & Methodius Church

Pobranie wymazu z policzka w celu wykonania badania

ภาพนิ่ง 1 - สำนักความร่วมมือระหว่างประเทศ

Robe spolupracuje s vítězkami tenisového Fed Cupu

Road Safety How can vehicle design play a role?

Preventing Stock Market Crises (V)

กฎหมายป องกันและปราบปรามการฟอก ที่มีผลกระทบต อธุรกิจ

Acanthocnemidae (Coleoptera), a family of beetles new to Russia

HABARI NJEMA - Resurrectionist

Biuletyn Bezpieczny Internet

Time to Phase Out Dirty Coal in South Eastern Europe

Klauzule zloupotrebe u potrošačkim ugovorima i ugovoru o osiguranju

Pronalaženje konkretnih rešenja za stvarne potrebe klijenata.

Regatna pravila

Stáhnout materiál (PDF)

xiv godišnje savetovanje udruženja za pravo osiguranja srbije

Devamı - kokhucrebulteni.com

Untitled - World Biennial Exhibition of Student Posters and

Kurumsal Eşitlik Endeksi 2014

Kosanović Rajko, Sindikalni leksikon, 2010

Proti praniu špinavých peňazí