Read

Gur

☰

Explore Categories

Sign in

Sign up

Upload

×

Download

No category

Pogledaj - Nova Banka

Pogledaj - Nova Banka

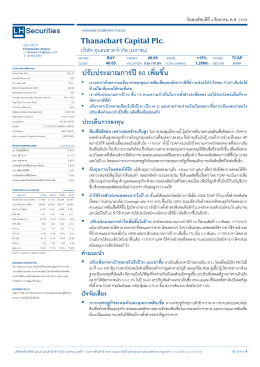

ปรับประมาณการปี 60 เพิ่มขึ้น

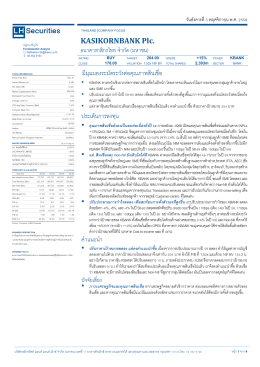

KBANK

Pogledaj - Nova Banka

Ročná správa / Annual report 2012

Vodic kroz zakonika krivicnog postupka kosova

full text

Godišnji izveštaj za 2013.

lista osób nagrodzonych w 40 międzynarodowym konkursie

Godišnji izveštaj 2010. - UniCredit Bank Srbija ad Beograd

Naučni časopis "Financing" - Broj 2 Godina 3 / jun 2012.

Pronalaženje konkretnih rešenja za stvarne potrebe klijenata.