Read

Gur

☰

Explore

Log in

Create new account

Upload

×

Download

No category

Mevzuat DeÄŸiÅŸiklikleri

Stručný návod pro instalaci a programování

yusuf baş yusuf baş yusuf baş yusuf baş yusuf baş

Antrenörlük Eğitimi IV - Beden Eğitimi ve Spor Yüksekokulu

43. Dönem Çalışma Raporu - Harita ve Kadastro Mühendisleri Odası

Ask Siirleri pdf free - PDF eBooks Free | Page 1

T.C. ESKİŞEHİR 3. (SULH HUKUK MAH.) SATIŞ

KPSS Maliye Öğrencinin Ders Defteri 2015 - TANITIM

Ä°dare KararlarÄ - Bursa SMMM Odası

Mevzuat DeÄŸiÅŸiklikleri

tc fat tc feke asliye hukuk mahkemesi 1 s ır a fa 2 3 4 5 6 7 8

Başımız Sağ Olsun - Bursa SMMM Odası

$UDPÖ]D +Rû *HOGLQL]

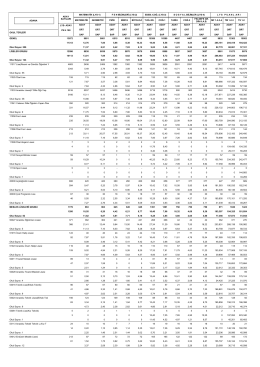

GENEL 13872 9801 9801 6515 6515 6515 10389 10389 4407

arslanlar elektrik fiyat listesi

![$UDPÖ]D +Rû *HOGLQL]](http://s2.readgur.com/store/data/000177352_1-21fe204fdf59fa9640e0fc30b7291dfc-260x520.png)