Read

Gur

☰

Explore Categories

Sign in

Sign up

Upload

×

Download

No category

Contacts Reciprocity Rule – List of Countries

dvoupodlažní elektrická jednotka 471 city elefant

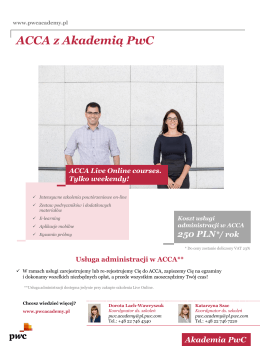

ACCA z Akademią PwC Akademia PwC

Szkolenia z zakresu audytu wewnętrznego i ryzyka Akademii PwC

Testowanie kontroli – teoria i praktyka

Izmene i dopune Pravilnika o PDV računima

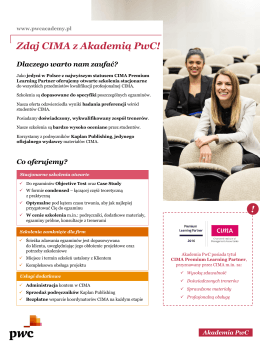

Zdaj CIMA z Akademią PwC!

Mapa metra a tramvají - Výluka Vodičkova

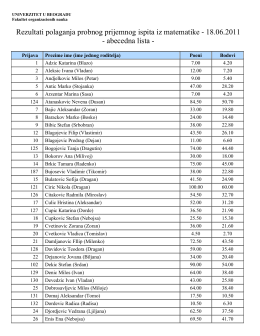

Rezultati polaganja probnog prijemnog ispita iz matematike

pwc Rachunek przepływów pieniężnych (Cash flow)

Szkolenia z zakresu obligatoryjnego doskonalenia zawodowego

Wzór badań (Matlab/Scilab)

Postersession_EEBST 2014 - Ecology and Evolutionary Biology