Read

Gur

☰

Explore Categories

Sign in

Sign up

Upload

×

Download

No category

Opportunities and Challenges of the EU Climate an

European Union Research in Foresight (2014)

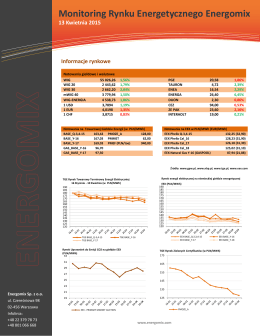

Tygodniowy Monitoring Rynku Energetycznego

Rozdzia l 8. Pojecie liczby porzadkowej

Remizy mogą działać uczciwie, a strażacy nic na tym nie tracą

W stronę nowego klimatycznego kompromisu

Propozycja-Współpr..

G.K. MEDPOL - canpol medsystems corporation

Gelişmekte Olan Ülkeler Küresel Sermayeyi Çekme Konusunda

Nilufer-Oral-COP-20-Limanin-Turkiye-Acisinda-Sonuclari-ve-2020

Europass Curriculum Vitae

SAMOEVALUACIJSKI IZVJEŠTAJ KATEDRE ZA HEMIJU I FIZIKU ZA

Marie Sklodowska Curie Bireysel Araştırma Bursları (IF)