Read

Gur

☰

Explore

Log in

Create new account

Upload

×

Download

No category

anti-dumping duty

Vaillant

In Devon, England Summer 2013 www.sol.org.uk

AD2007 amending AD2006

preuzmi ovaj dokument

Bu sayfaya ait ilgili dosyayı indirmek için lütfen buraya tıklayınız

AD2006 - Gov.uk

örnek yeterli̇k sinavi

Program Booklet - Bilkent Senfoni Orkestrası

1-6 Temmuz 2014 Haftası Denizcilik Haberleri

Document

DIŞ TİCARET ENSTİTÜSÜ Ticari Diplomasi (Tezli/Tezsiz) Yüksek

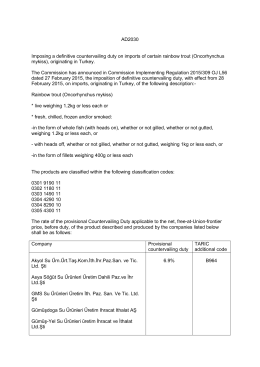

AD2030 Imposing a definitive countervailing duty on

Discrimination Cases Report - Final.pdf

CeBIT BİLİŞİM EURASIA

Antalya-Kemer-Tekirova Güzergahında Açılan Altan Ayağ Tüneli (T3

4 September, 2014 EXHIBITORS GUIDELINE

30 JUNE 2013 An insight into the work of the

20 - Pravdepodobnosť

AGB Deutschland

Tam Metin - Kalem Uluslararası Eğitim ve İnsan Bilimleri Dergisi

Giriş - Osmangazi Üniversitesi İktisadi ve İdari Bilimler Fakültesi

Nilufer-Oral-COP-20-Limanin-Turkiye-Acisinda-Sonuclari-ve-2020