Read

Gur

☰

Explore

Log in

Create new account

Upload

×

Download

No category

KBC Eco Fund

KBC Select Immo - BKB Bank – Bremer Kreditbank AG

folder - Kopalnia Inspiracji

NADAWCZE STEMPLE JEDNOWIERSZOWE UśYWANE PRZEZ

Včtací systém ZOBO 3 31–50 mm

les emplois de la semaine - Far North East Training Board

On Wall Street

pozrieť v tomto PDF. - Ako

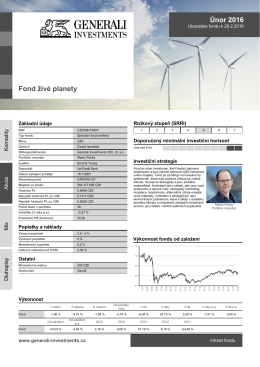

Fond živé planety ČP INVEST

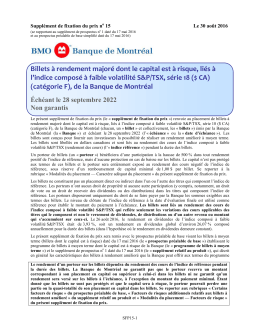

Billets à rendement majoré dont le capital est à risque, liés à l`indice

Všetci sa boja - financialnews.sk

poradenství & finance poradenství & finance 12/2013

Výsledky kultivácie rias

KATALOG - Young Architect Award

Billets à rendement majoré dont le capital est à risque, liés à l`indice

Stáhněte si č. 19 v PDF - Česká společnost pro údržbu

Zmiana systemu wsparcia dla OZE

Kobanê halkının yanındayız!

Roztáčíme kola Vašeho podnikání - ČSOB Leasing pojišťovací makléř

BORUSAN YATIRIM VE PAZARLAMA A.Ş. Eylül

Mišljenje revizora, napomene i finansijski izveštaji za

Tam Yoğuşmalı Kazan

FAALİYET RAPORU 2013