Read

Gur

☰

Explore

Log in

Create new account

Upload

×

Download

No category

Modelling and Forecasting Inflation Rates in Ghana

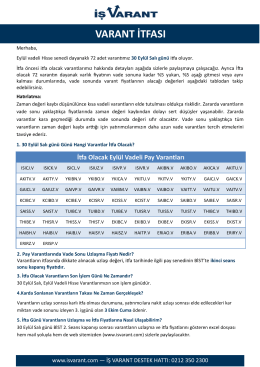

varant itfası

tematika

Ecsetkatalógus

aihm içtihatları çerçevesinde özel hayata ve aile

Nr 1/2013 – Afr - Przez Pryzmat Praw Człowieka

burayı

UDHËZIM ADMINISTRATIV Nr. 01/2013

18. Uçan Süpürge Uluslararası Kadın Filmleri Festivali 8

Geniş QRS

Application of Harberger-Laursen-Metzler Hypothesis

pdf dokument

SWEMP 2016 October 5-7, 2016 Istanbul Turkey FIRST

Full Text - Journal Of Business Research

Odborný posudek vedoucího diplomové práce

program Bihtel 2010

infrastruktur publik dan pertumbuhan ekonomi indonesia tahun

Modelovanie a prognózy vývoja vybraných ukazovateľov trhu práce

Jeseň 2012 - Slovenská asociácia podnikových finančníkov

Hassas Nokta Konumlama Tekniği 2013

BAB I PENDAHULUAN A AKANG MASALAH LATAR BEL Di era

การใช้ Repetitive Sequence-Based PCR (rep